- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- Carta Scrapped Secondaries – Good News, You Can Still Access the Secondary Ecosystem

Carta Scrapped Secondaries – Good News, You Can Still Access the Secondary Ecosystem

a newsletter about VC syndicates

Zachary Ginsburg & Alex Pattis

January 17, 2024

Last Money in is Powered by Sydecar

Sydecar is a frictionless deal execution platform for emerging venture investors. We make it easy for anyone to launch SPVs and funds in minutes, with automated banking, compliance, contracts, tax, and reporting so that customers can focus on making deals and building relationships.

Carta Scrapped Secondaries – Good News, You Can Still Access the Secondary Ecosystem

One of the big news stories over the last month was that Carta was ending Carta X, following controversy over its use of customer data. The company faced allegations that it used confidential information to solicit investors in startups, leading to a breach of trust and privacy concerns. Carta's CEO, Henry Ward, acknowledged that the company had "done a decent job at building the cap table business" but "an abysmal job at the secondary business." The decision to exit the secondary market business was made to prioritize keeping customer data private and to address the breach of trust. The move was also seen as removing a potential conflict of interest.

This is net bad news for Carta, but candidly has minimal impact on GP/LPs ability to access secondary investment opportunities and investors/employees/founders ability to sell their private market stakes. Accessing the secondary markets is actually quite easy today via marketplaces, aggregators and SPVs.

One of the hottest parts of the SPV market right now is the late stage secondary market, where there’s higher assurances of a company entering the public market and information/access asymmetry has enabled GPs to find great deals if they know what they’re looking for.

So as an LP/GP, how do I find these opportunities?

SPVs:

One of the best ways to access this ecosystem is via venture and angel Syndicates/SPVs. There are many active syndicators frequently running allocations for secondary investments including into highly sought after secondaries such as SpaceX, Anduril, Brex, Canva, Kraken, Circle, Ramp and many others. There’s some good and bad to this for LPs, who access these opportunities via SPVs.

The Good:

Low investment minimums - many SPVs only have minimums of between $1k-$25k commitments (some are higher), but overall a very low relative minimum investment threshold to access the late stage market. This is great as SPVs essentially democratize access to any accredited investor given the low minimum investment threshold.

Minimal LP efforts required - the SPV GP is doing the work on sourcing and diligencing opportunities and putting together the marketing materials, leaving an LP with minimal effort/friction to invest and access these otherwise difficult to access/evaluate businesses.

Best pricing/negotiating - the SPV GP is typically doing everything in his/her power to source and negotiate the best pricing on a secondary. This can sometimes take a large amount of effort that LPs don’t have to deal with.

The Bad:

Carry: By putting the effort on the GP to source, diligence, negotiate and market an allocation, you will likely be paying fees & carry to that GP for his work. This typically ranges between 10-20% carry. There are also management fees typically associated with these vehicles of 10% to 20% over a ten year period.

Liquidity: If you were to buy a secondary investment directly and be on the cap table, you then have full discretion on when to sell your position once your position freely trades on a public market. That right is typically taken away when you invest in an SPV as the GP is the advisor/manager of the SPV. While GPs sometimes sell positions when the lockup period ends, some GPs hold positions longer even if the shares are freely tradeable because he/she may feel the position is undervalued.

Fund Admin Fees: In addition to carry & management fees provided to the GP for running the secondary, the fund admin is typically also charging some small fee amounts, though candidly it is usually negligible for large secondary SPVs.

Introducing the marketplace for private stock

Whether you run a fund, lead an investing syndicate, or invest solo, Hiive gives you unparalleled access to some of the most exciting private companies. With over 700 closed transactions totaling over $300M across 140 unique issuers, Hiive is the fastest growing pre-IPO marketplace in the world.

Secondary Marketplaces & Brokers:

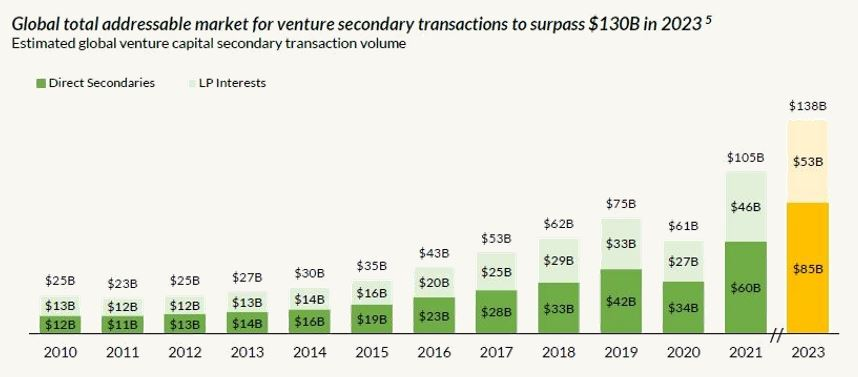

The secondary market has ballooned over the last 15 years, which has led to an enormous number of entrants building software and marketplaces to facilitate secondary transactions. According to a report from Industry Ventures, the global addressable market has ballooned from $25B in 2010 to an estimated $100B+ at peak.

According to that same report, “Since the inception of Industry Ventures in 2000, the venture capital asset class has grown over 10x in size. Institutional and high net worth investors continue to grow their commitments to venture capital in search of alpha and to gain exposure to the fast-growing technology sector. As a result, traditional venture capital firms raised over $1.7 trillion over the last 10 years, compared to just $406 million over the prior 10 years. We have also tracked an exponential increase in the number of venture capital funds being formed each year. From 2016-2021, a whopping 12,600 new venture funds came into existence. This was more than 2x the 6,100 funds formed across the prior six years, which was again more than 2x the 2,700 funds formed across the prior six years. The growth of the primary venture capital market is fueling the secondary market with supply of sellers and investments.”

In other words, with the venture capital industry booming and private startups staying private longer, the demand and need for secondaries on both sides has exploded, which has led to the emergence of extremely active secondary marketplaces.

One of the first large secondary markets to come on the scene was SecondMarket. Barry Silbert – who later started Digital Currency Group - is known for founding SecondMarket, which was later renamed to "Nasdaq Private Market." SecondMarket was created in 2004 and became the largest secondary market for private-company shares, including hot-ticket names like Facebook, Twitter, and Dropbox.

The secondary marketplace ecosystem has become much larger (and fragmented) with the emergence of a number of platforms including Hiive, Zanbato, Forge Global, EquityZen, Setter Capital, and others. There are differences in how these marketplaces operate.

Hiive has created its own website marketplace where buyers/sellers can place bids and asks for companies and Hiive will facilitate those transactions for a fee. Other marketplaces like EquityZen may sign a supply of an allocation and then list those allocations on their marketplace to be filled on a first come first serve basis.

"A big issue in the secondary market is trust— participants seldom know if an opportunity presented to them by a broker is in fact real, or if the broker is fishing for a buy or sell order. Our marketplace tackles this problem by enabling users to bid, negotiate, message and ultimately match on a trade, directly with each other. Once they agree on a deal, Hiive communicates with the issuer for approval, and finally executes the transaction." — Sim Desai (CEO, Hiive)

The Good:

Easy Access: Brokers and secondary marketplaces have done a fairly good job of aggregating supply and demand in the secondary ecosystem. This makes it easier for SPV GPs, Funds and large HNW individuals to access high in demand companies.

Reducing Friction: These marketplaces also typically work with the IR/C-Suite at the startups listed on their platform to coordinate and handle transactions, providing a higher level of assurance that the secondary transaction will go through and overall take some of the coordination pain out of the process.

Market Knowledge: These platforms usually have difficult to access info to ensure a smoother transaction such as the ROFR price (right of first refusal - contractual right that gives a party the option to enter into a transaction before anyone else can), any restrictions or requirements on secondary sales, among other key pieces of information that could blow up a secondary deal during closing. Getting rofr’d at the last second is a horrible experience for buyers, so having assurances on what the accepted market clearing price is for a company and their ROFR info is very helpful.

The Bad:

Loose Practices: Candidly, these markets still have some work to do to create efficiencies. Often supply/demand for hot secondary names is a moving target with supply there one second and gone the next. The best marketplaces I have found have sellers sign LOIs that give GPs exclusive access to buy their supply for a specific period, but a few are still playing fast and loose with supply/demand (e.g. telling a buyer they have supply at x price, when they don’t and rather are stating they do to just try to make a market), which can make the experience frustrating for buyers and syndicators.

Fees: Secondary marketplaces charge fees for service. Marketplaces like Hiive have made it a point of emphasis to only charge seller fees, while marketplaces like Forge typically charge buyers and sellers. Fees should be expected as these marketplaces need a viable business model, but if you’re a seller (and buyer potentially) expect to pay 1-5% of the transaction for brokerage fees.

Fragmentation: This ecosystem is extremely fragmented among many marketplaces and brokers - finding the best pricing requires significant effort and is not streamlined well enough across these marketplaces. This means GPs are typically interacting with many brokers/marketplaces trying to source and negotiate the best price.

Broker Aggregators

As mentioned, these marketplaces have some work to do today to create a more optimal experience for the ecosystem, which has recently led to the rise of aggregators. One name that has recently garnered some traction is Caplight, which you can think of as an aggregator for the secondary market.

Caplight consolidates opportunities from over 50 broker-dealers to provide an aggregation layer of supply/demand across the secondary broker/marketplace/LP ecosystem. Caplight also has products that track completed secondary deals, offering users a real-time view of how investors are valuing companies

“Our model is similar to Zillow’s - we try to show investors all of the ‘listings’ (available buy/sell opportunities) from across the market. If you’re interested in buying/selling, we connect you with the ‘agent’ (one of our broker partners), who will complete the transaction with you. This tool is necessary because the different brokerages in the secondary market offer unique deal flow and many investors don’t want to have to constantly check in with all of them.” – Javiar Avalos (CEO of Caplight)

The Good:

Single Source of Truth: By attempting to aggregate the secondary space, efficiency should be driven to the market both in the form of liquidity and best pricing. By also providing a data layer of recent transactions, participants can also get real time data on where companies are trading on the secondary market.

Potential Free Costs: Caplight has a unique model where they charge an upfront SaaS fee for buyers for access to its tools and marketplace; if you’re active on the marketplace, it’s possible you won’t pay any buyer fees as the upfront fee is refunded with usage. This offers the potential to pay no subscription fees when purchasing secondaries on Caplight

SPV Tools: Caplight has some helpful tools around helping SPV leads fill allocations, specifically if you’re running an SPV for a company, Caplight can introduce you to potential buyers to invest in your syndicate, where you can take fees & carry.

The Bad:

Upfront Fees: Distinct from many secondary brokerage firms (and as mentioned), Caplight charges $15,000 upfront for a software subscription to its service, which is refunded over time if you transact on Caplight. It requires approx. $1.5M in transaction volume per year on Caplight to get this $15,000 fee completely refunded, which is fairly easy for an SPV, Fund or other participant, though it may be harder for a HNW individual. However, if you don’t end up transacting on the platform, Caplight keeps the entire $15K SaaS fee.

Not Every Broker Joins: Notably there are secondary marketplaces that have not joined Caplight yet, meaning buyers may still have to potentially work with other marketplaces if Caplight doesn’t have supply and/or check other marketplaces for better pricing.

Adverse Selection: It’s possible that brokers can move high in-demand companies fast (very hard to get names) and thus that supply won’t make it on Caplight, leading to the potential of adverse selection, though from what I’ve seen Caplight has a fairly comprehensive offering.

Funds:

Over the past decade, a number of large secondary buyers have emerged, including family offices, sovereign wealth funds, and pension funds, expanding the pool of potential buyers and sellers and increasing liquidity in the market.

As one example, Industry Ventures is a pioneer in the venture capital secondary market, raised $1.4 billion for its latest flagship secondary fund, making it one of the largest dedicated venture secondary funds ever raised. Secondary funds are becoming extremely common. I won’t dive too much into this in this article but these funds are usually very difficult to access for small accredited investors given the sheer size of these vehicles. If you’re a smaller investor (putting $10k-$1M to capital to work), you’ll likely find it much easier investing via SPVs/brokers.

To Conclude:

There are a lot of ways to access the secondary market ecosystem via marketplaces, brokers, SPVs, aggregators and funds. CartaX was apparently a very small business only doing ~$3M a year in revenues, so despite its high profile nature, its exit doesn’t leave much of a gap, though its potential was exciting.

I’m personally curious to see how other fund admins like AngelList, Sydecar, and others approach the ecosystem as there may be a big opportunity for them to make a market given the sheer number and dollar volume facilitated on these platforms, though to be determined.

Alex is on the VC10X Podcast

Peter Walker on Benchmarking giving equity to advisors

Last Money In is Powered by Sydecar

Sydecar is a frictionless deal execution platform for emerging venture investors. We make it easy for anyone to launch SPVs and funds in minutes, with automated banking, compliance, contracts, tax, and reporting so that customers can focus on making deals and building relationships.

How did you like this weeks topic? |

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!