- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- Why High Fees are Pinching the SPV Market

Why High Fees are Pinching the SPV Market

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

January 31, 2024

Last Money in is Powered by Sydecar

Sydecar is a frictionless deal execution platform for emerging venture investors. We make it easy for anyone to launch SPVs and funds in minutes, with automated banking, compliance, contracts, tax, and reporting so that customers can focus on making deals and building relationships.

State of SPVs - Why High Fees are Pinching the SPV Market

I’ve been syndicating venture capital investments since 2020 with >400 SPVs closed, and have been a part of the ecosystem on the LP side for several years prior to that. Given this, we’ve had the unique opportunity to see a normalized bull run (2017-2020), the covid downturn (2020), the post covid boom (2020-2021), the post covid bust (2022-2023), and now the very slow return to normalization (2023) in the SPV ecosystem.

What the ecosystem looked like during each of those periods:

2018-2020 (before covid) – optimistic normalcy: deals we’re getting done with the syndicate ecosystem overall healthy with a limited amount of emerging managers, full time syndicators, emerging GPs running sidecar SPVs

2020 (covid) - temporary intense fear and uncertainty: more or less the same as pre-covid albeit everyone slowed down for a few months to better assess the covid damage

Late 2020 – 2021 (post covid boom) - irrational exuberance with ZIRP and cheap money: there were probably a dozen active managers I followed in the pre-covid period. That number swelled to well over 50 active syndicate GPs in the post-covid boom period. My inbox was filled with on average probably 3-7+ new venture deals every single day, and most were raising a lot of LP capital.

2022-today (post covid bust) – anger, grief, disinterest: slowly over the last 18 months, the ecosystem has slowed into only a very small handful of extremely active syndicators (40+ SPVs/year) and relatively small handful of folks who actively syndicate otherwise (excluding full time large VC funds who run sidecar co-investments for their LPs). I’d say almost ¾ of the syndicators I saw during the 2021 period have more or less disappeared e.g., syndicating <5 deals/year, left the ecosystem entirely.

Part of the reason for the 2022 downturn in the SPV market is known and obvious. ZIRP market in 2021 led to a boom in capital invested in venture, much of which was invested with less than optimal diligence and/or into companies at hugely inflated valuations and/or sub-par businesses. LP realization that they shouldn’t be paying valuation premiums for illiquidity or investing into managers that we’re playing loose with LP capital. Additionally, poor performance of recent IPOs and unicorns in public markets crashed due to spike in interest rates, completely stalling the venture growth markets, etc. etc. etc.

However, in the second half of 2023, public markets started to boom with the Dow hitting an all-time high. And despite that, the venture market has been lagging (arguably very normal and expected), but the syndicator market has shown much less sign of recovery and investment interest is still massively depressed (excluding sidecar SPVs from established funds).

This has made it hard to get SPVs done and has led many syndicators to leave the ecosystem despite the boom in publics and return to normalization in some parts of venture. Those that are still active are probably doing 10-20% of the number of deals they were in 2021 and investing a fraction of capital into each due to depressed LP interest.

Introducing the marketplace for private stock

*Investing in private securities involves a high level of risk.

Whether you run a fund, lead an investing syndicate, or invest solo, Hiive gives you unparalleled access to some of the most exciting private companies. Better yet? Buyers don’t pay fees. With over 800 closed transactions across more than 150 unique securities in 2023, we are the fastest growing pre-IPO marketplace in the world. Create a free account today to see why the top investors trade on Hiive.

So what is depressing the venture SPV market if publics are skyrocketing and risk appetite seems on again?

For one, there’s a general sourness and disinterest in the asset class following the poor deal quality and bad behavior that ran rampant in 2021, among the other factors discussed above. This is candidly the #1 reason. But the other part of it is the high fees associated with running smaller SPVs.

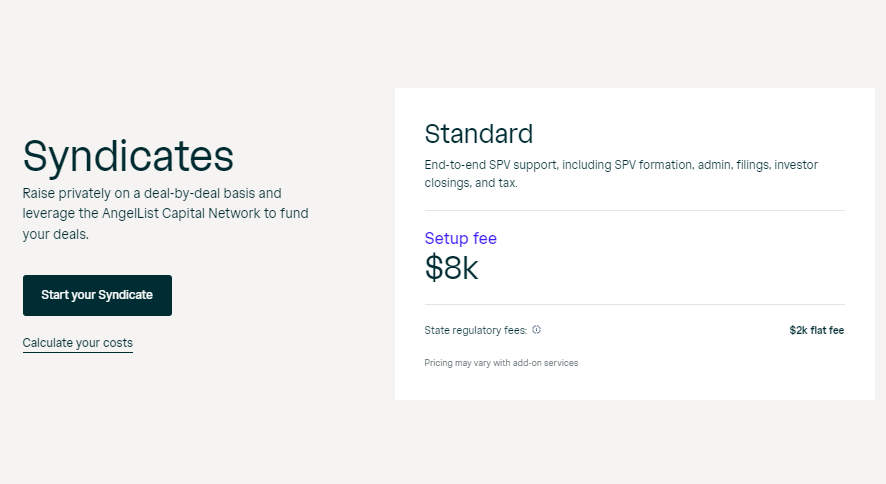

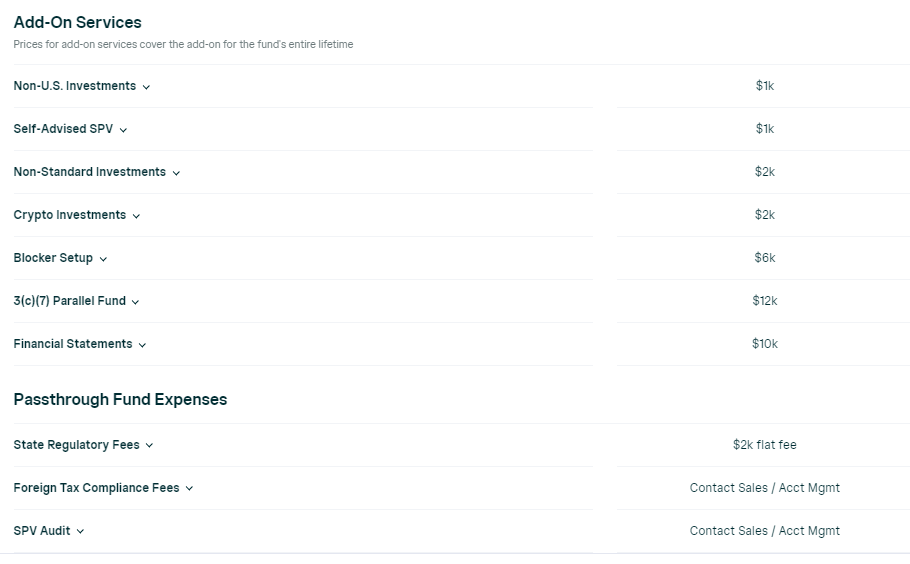

The most cost effective way to run SPVs nowadays is through tech-enabled fund administration platforms including AngelList, Sydecar, Canopy, Carta. But, even with these platforms, fees are often upwards of $8,000, which makes putting together small SPVs (<$75k) difficult if not untenable.

Many syndicates, especially those just starting out or investing at the early stage, may only be able to raise $50-100k from their investors. Some fund admin platforms do not want to charge LPs in an SPV more than 10% of the SPV as SPV pass through fees. Meaning if your fund admin charges $8k in fund admin fees, on a $40k SPV deal, a GP may only be able to charge their LPs $4k (10% x $40k = $4k) and the GP has to put up the remaining $4k out of pocket. Some fund admin platforms allow GPs to pass through more than 10%, but in either case, that’s not a good experience for the GP/LP when that happens.

And this is a big problem. Very few emerging GPs don’t have the cash to front admin fees and LPs understandly don’t want to pay more than 10% of their investment in fees.

Smaller deals (<$100k) have become more common in this market, and syndicators have become frustrated by rising transaction fees that result in canceling SPVs altogether. This has not only led to less deals getting done but a complete behaviour shift in top of the funnel for GPs – many GPs now won’t even bother with syndicating a deal unless they have high confidence they can fill it.

***You may be thinking this is a good thing for LPs because it will lead to a higher quality of deals being presented by GPs. In reality, the result is that GPs are only syndicating the highest signal deals (e.g. tier 1 co-investors, large brand names), which doesn’t translate directly to quality. Speaking from personal experience, some of our best early stage deals are ones that don’t end up getting syndicated because they are too early to be on a top VCs radar.

However, there are some solutions coming up.

We use and enjoy AngelList, and they are constantly pushing the envelope in terms of developing better software and tools for GPs, but they are aware pricing needs to be a bit more competitive to allow very small SPVs to get done. They have robust marketplace features as well to help GPs get started attracting LPs.

Right now AngelList charges $8,000-$10,000 (approx.) for end-to-end SPV support, including SPV formation, admin, filings, investor closings, and tax. AngelList also takes 5% carry on AngelList LPs. There may be add-on fees depending on other factors including company HQ, token deals, among others. Pricing is typically ~30% less for follow-on SPVs. More pricing details below.

We’re also excited about Sydecar’s SPV platform. Their standardized approach to SPV formation and admin allows them to price more competitively while still offering a reliable, best-in-class experience.

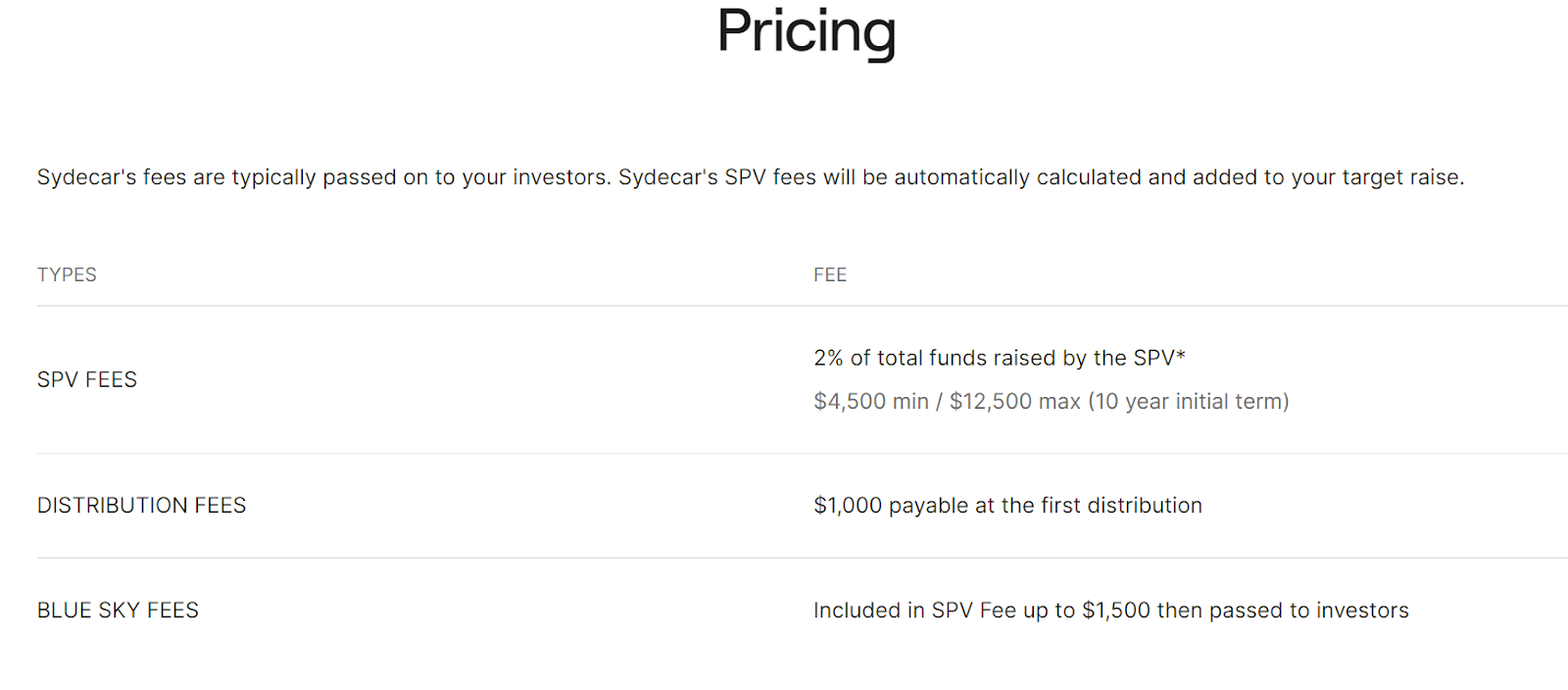

Sydecar's SPV fees are 2% of the total funds raised by the SPV. The minimum fee is $4,500, and the maximum is $12,500 for a 10-year initial term. Their fees are all-inclusive, so GPs won’t be surprised by additional pass-through fees when they’re ready to close their SPV. The $4,500 minimum and price transparency allow GPs to get more deals done without paying out-of-pocket fees. Sydecar also doesn’t take a portion of the upside (carry) from an investment.

Not only is Sydecar’s approach good for GPs, but it also gives LPs more exposure to the underlying investment rather than having their capital go to transaction fees. We know the Sydecar team well and consistently hear very positive feedback about their product and the team from other GPs and syndicate leads.

We asked a few Syndicate/Fund GPs the following questions:

Do SPVs have too high fund admin fees; if yes, what are your fund admin fees per deal (in $) typically?

Are SPV fund admin fees preventing you from getting deals done?

Are high fund admin fees leading to behavior change at all in running SPVs in general (e.g. you don’t believe you’ll be able to cover fund admin fees on many deals so are not even trying to syndicate any deal that you're unsure you’ll be able to close)?

Any other thoughts on this topic?

Jonathan Wasserstrum - Founder and Partner at Unwritten Ventures:

“Fees — and especially the fee increases as LP demand is slowing — are resulting in us bringing fewer deals to the platform. We don’t like running deals that we can’t close, it’s a bad experience for the company and LPs. Unless a company has a brand name VC leading, it’s challenging to raise enough to close a syndicate. Perversely these deals wind up being the more interesting and oftentimes better performers over time. These days we just do from our fund which works out for those LPs but not for broader platform LPs.”

Ohad Gliksman - Managing Partner at 5eyes

Regarding your questions on fund admin costs, I tend to think the fund admin costs make sense. In the opening lecture of economics 101, the lecturer told us: If you're going to take a single lesson from this course, let it be that there is no such thing as a free lunch.

While fund admin costs on Angellist and other platforms I've looked at quote at around $10K, I think the cost is fully justified. The only place where this is a concern is when the actual SPV size is low (around $100K) which means the admin takes a big chunk of the actual investment.

From my perspective, the fact that the platforms focus on many deals with low LP commitments makes our syndicates less effective in the broader sense of the venture capital world. If I had the ability to do so, I would set the SPV minimums at $200K removing a lot of the less meaningful investments since I don't see them serving us or the founders in the long run.

Confidential GP (requested anonymity, but gave us permission to include)

Do SPVs have too high fund admin fees; if yes, what are your fund admin fees per deal (in $) typically? My biggest issue with the fees is that I don't think syndicate GPs should be on the hook for paying the remainder of the 10% if the raise is less than $80k.

Are SPV fund admin fees preventing you from getting deals done? There have definitely been a few this year that could have closed at +/- $60k in < 6 weeks but ended up taking 3+ months to get to the minimum.

Are high fund admin fees leading to behavior change at all in running SPVs in general (e.g. you don’t believe you’ll be able to cover fund admin fees on many deals so are not even trying to syndicate any deal that your unsure you’ll be able to close)? I don't think so…what is changing my behavior is the difficulty creating any meaningful relationships with LPs on AngelList and the lack of ability to charge management fees.

Any other thoughts on this topic? Just that I think the syndicate GP user experience has continued to get worse and worse while the fees have gotten higher and the LP demand has gotten worse.

Confidential GP (requested anonymity, but gave us permission to include)

“Off the record -- screw fees — or more specifically the increase. Fees used to be 8k, now it's 10k. They used to give fee breaks for deals you were also doing from a fund but that’s stopped. At the same time they were raising fees for the fund too. It seems shortsighted for AL [AngelList] to be increasing fees at the same time volume is down the platform. This makes for a worse experience for both leads as well as LPs.”

Rounding out this post

GPs: Work with the fund admin platform that best fits your needs. AngelList provides an incredible experience and full service operation with somewhat reasonable fees (albeit not ideal fees for small SPVs). Alternatively, Sydecar provides a reliable, product-driven solution with very competitive pricing in the industry, making it more feasible to run smaller SPVs. Evaluate both to determine which is best for your needs. Let us know if you’d like an intro to either of these fund admins.

LPs: Unfortunately you’re seeing less deals. You may be happy about that, but I’d argue this is worse for you as you’re likely seeing the highest signaling opportunities, but perhaps not the deals that can really make you the 100-500x (Uber like upside) as those deals may be before a tier 1 comes in.

If you like this article, check out our other articles that cover related topics

Last Money In is Powered by Sydecar

Sydecar is a frictionless deal execution platform for emerging venture investors. We make it easy for anyone to launch SPVs and funds in minutes, with automated banking, compliance, contracts, tax, and reporting so that customers can focus on making deals and building relationships.

How did you like this weeks topic? |

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!