- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- Venture Capital SPVs - a Decade of Delayed Gratification

Venture Capital SPVs - a Decade of Delayed Gratification

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

March 20, 2024

Last Money in is Powered by Sydecar

Sydecar is a frictionless deal execution platform for emerging venture investors. We make it easy for anyone to launch SPVs and funds in minutes, with automated banking, compliance, contracts, tax, and reporting so that customers can focus on making deals and building relationships.

Deal Sheet = Deal Flow Just Got Better!

Curated & Discounted SPVs directly to your inbox

Deal Sheet is a paid weekly newsletter that delivers the best startup investment opportunities weekly. These deals are being syndicated by 20+ of the best and most active syndicate leads we’ve worked with. All Deal Sheet deals include discounted carry (10% carry versus standard 20%).

On Monday, we shared five startup investment opportunities via Deal Sheet. The deals included were:

Deal #1 → Series A company building the Plaid for point of sale (POS) transactions

Deal #2 → Pre-IPO revolutionary cybersecurity and data management company acheiving more than $1.5B in Revenues and backed by Lightspeed, Greylock, Khosla, Bain Capital and others

Deal #3 → A Unicorn Beverage company that achieved $263m in revenues last year (special 0% carry for subscribers for this deal)

Deal #4 → Enterprise technology company building the AWS for Restaurants backed by a confidential top tier fund

Deal ex. #5 → A luxury Gin company co-founded by a major Celebrity with 75M followers across social

***If you are interested in becoming a Deal Sheet subscriber, but want to chat further, email us here directly ***

Venture Capital SPVs - A Decade of Delayed Gratification

The average timeline for a company to go public through an initial public offering (IPO) is typically between 7 to 10 years from its founding date. That means if you’re a Seed stage VC, you’ll very likely have to wait a decade to see any amount of meaningful carry (profit) from your investments.

That’s a tough pill to swallow and underscores the disconnect between public perception of how well off many new VCs are and the reality of their income, which isn’t meaningful from SPV activites typically for many years with often a decade of delayed gratification. We previously put out an article discussing what $200M AUM in VC syndicates look like - in the near term, it’s not too lucrative.

For multi-hundred to billion dollar funds, there is a similar delayed gratification of realizing carry profits, but it’s likely not felt nearly as much as General Partners (GPs) of large funds can receive near seven figure incomes or more absent carry just from management fees alone. For emerging managers with smaller funds (<$100m), you can still usually collect a six figure salary, which allows some certainty of income with a steady paycheck while you await hopefully significant carry on the backend (7-10+ years out).

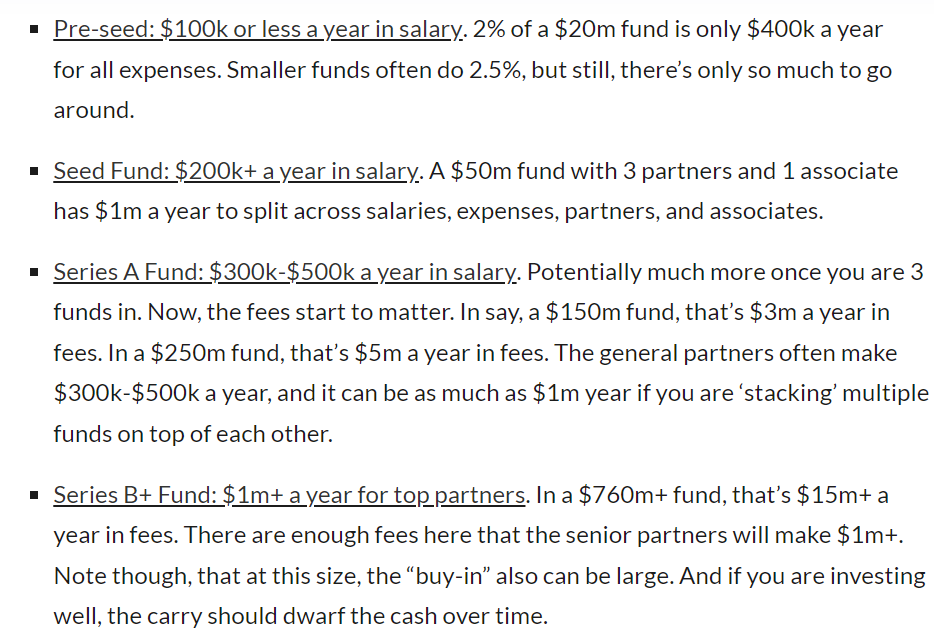

Jason Lemkin of SaaStr put out some rough guidelines on what GPs typically make at different fund stages/sizes, which I’m including below for reference.

“You can also see from this why many VC firms now are raising new funds every 2 years (vs 3–4 years before). These fees start to “stack” on top of each other to some extent, and thus, your salary can double (along with your gains).”

To summarize Jason’s point, small, early stage VC fund GPs are making minimal actual salary as there’s not much in fees to go around, but nonetheless they often receive a salary. Larger funds can generate substantial fees in the many millions, and once you have multiple funds closed, those fees stack as GPs receive fees from funds long after their deployment period for new investments.

For an SPV lead however, you have to get extremely creative, because as mentioned across prior articles including the one here on Should SPV Leads Take Management Fees, many SPV leads do not take management fees, and often have to figure out alternative ways to generate income while they await carry (hopefully) a decade out.

I personally generate income in the interim primarily through consulting fees, small amounts of carry realized from our firm growth deals/small exits and prior personal investments and public investing. We just had one of our portfolio companies Jackpocket exit for $750M to DraftKings as one example. We have previously had portfolio companies including Bear Flag Robotics, Inkbox and others also get acquired that netted nice carry in the interim. I’m also starting to see some income from Last Money In, but today, we’re reinvesting almost all of our newsletter income back into Last Money In.

Without disclosing any names, here was our best realized investment from our firm within four years of starting it. Of note, there are many companies marked up substantially, but those investments are not realized with no certainty of future performance.

The SPV raised $416,000

Company exited with proceeds back to investors of $3,609,964 in cash

1 year after exit, earnout payment of $412,233 for total payment of $4.0M

Total carry on this deal was about ~$540,000

We typically have scouts or partners who receive carry, but on this one we didn’t. The deal was sourced through a referral from a portfolio company

Needless to say, the major income generating events are expected to come from 7-10+ years of compounding our best investments, and with that we’re still likely a few years away from seeing the potential of multi-seven figure carry outcomes. The net for many full time SPV leads is often effort for 1-7+ years without any meaningful income (often) or certainty of any meaningful exit at all, and that wears on many SPV leads. It’s part of the reason for the turnover in this ecosystem.

Brought to you by Hiive.

*Investing in private securities involves a high level of risk.

Whether you’re a fund manager or solo investor, Hiive gives you access to some of the most exciting private companies in AI and Web3, including the likes of Anthropic, Liquid Death, Kraken, Ripple, and Groq. Better yet, you get troves of historical pricing data based on real user activity across hundreds of the top unicorns for free.

Create an account today and learn why thousands of the top investors trade on Hiive.

So how do most SPV leads generate income?

Management fees on SPVs

Start a Rolling Fund or Traditional Fund (collect fees)

Pivot to working for a VC fund (guaranteed salary)

Advise or consult for companies

Carry from fast exits (e.g. our example above)

Carry from secondary investments (i.e. sell stake in existing portfolio companies when marked up, but before a liquidity event)

Non VC investment income (stocks, crypto, etc.)

Sell portfolio companies on value add with affiliate fees attached to them

Do SPVs part time and generate income through a separate FT/other role

Many SPV Leads actually don’t do SPVs full time because of this lack of income. We put out a post discussing this, and I’m reposting some of their replies again below:

Jeroen Bertrams: Doing SPVs almost full time at the moment. While the number of deals is down a lot, I still spend lots of time chatting with founders, helping portfolio companies and trying to find the right deals; next to SPVs I do some direct investments as well and I'm writing a new book :)

Devon O’Rourke: I founded and run a tech product marketing consulting firm, Fluvio. We're the firm tech companies turn to with their most strategic, critical go-to-market challenges. We have worked with the likes of Amplitude, Stack Overflow, ABC Fitness, Moneylion, Nasdaq, eBay, G2, and many more.

Yash Godiwala: I work on Growth Product at Ramp.com, NYC's fastest growing startup. Through leveraging data, high-quality engineering, and a velocity-first framework, our team builds software that generates bottom-line revenue.

Justin Smith: I run venture investments at Recharge Capital, a thematic asset manager focused on global innovation in fintech and healthcare through a blend of private equity and venture capital strategies.

Joseph Turner: CFO for growth companies across deep-tech.

Bradley Mullen: I've been a radiologist for 15 years and it is the perfect specialty for a physician interested in the intersection of medicine and technology. Radiology is one of the specialties pushing the bounds of technology in medicine, beginning with the earliest adoption of fully digital information systems, later voice recognition, and now moving into some of the most mature uses of AI in medicine at the moment.

Elana Dickman: Outside of running SPVs for Red Beard Ventures, I also manage Red Beard Ventures Fund I which is a full-stack web3 fund investing across blockchain consumer applications, infrastructure, gaming, the metaverse, and DeFI, in both equity and tokens. I also spend a lot of time on our tokenomics accelerator Denarii Labs, which is in partnership with Horizen Labs Ventures and Red Beard Ventures. I am also the co-founder of The Girls Table a social media platform that amplifies entrepreneurs, creators, and investor's voices through a podcast, newsletter, IRL events, and a private chat.

Matthew Wilson: I never intended to make Allied a full-time job, but it's how things worked out as a result of the pandemic. When I'm not running an active SPV, I spend most of my day networking with founders and other investors––you never know where the next great opportunity will come from. If it's a super slow day at the office, you can find me on the bike trails or ski slopes.

Colin Gardiner: Outside of running SPVs I spend all my time advising and consulting marketplaces and platforms. I am a marketplace geek and try to write as much as possible about them at gardinercolin.com. Working and writing about marketplaces is also my largest source of deal flow as founders come to me for help and advice. I am creating a new SaaS product for marketplaces/platforms called Longtail that allows them to create 100-1000s of SEO pages in days vs months.

In any case, running SPVs is an ultimate form of delayed gratification, and I may get push back on this, but potentially even more so than VC backed founders as they typically have a salary from VC funding and can in some cases (especially at the growth stages) have a very meaningful salary. Though I also personally know many founders who pay themselves near nothing and work 80-100 hour weeks for almost entirely sweat equity - I give the world of credit to those founders.

Once the 7-10 year hold period is finally realized, many GPs certainly expect to see large ongoing checks as theoretically they’ll begin to see an ongoing stream of their best first check companies reach IPO level scale, and even quick outcomes can net many of us multi-six figure income in the near term, so I guess it’s not all that bad.

If you liked this article, check out our other articles:

Last Money In is Powered by Sydecar

Sydecar is a frictionless deal execution platform for emerging venture investors. We make it easy for anyone to launch SPVs and funds in minutes, with automated banking, compliance, contracts, tax, and reporting so that customers can focus on making deals and building relationships.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!

✍️ Written by Zachary and Alex